İrem Kalender

The Formula That Changed Wall Street

Some ideas don’t just explain the world — they quietly reorganize it. The Black–Scholes model is one of them. It took something that once felt speculative and imprecise, and gave it a structure precise enough to build an entire market on.

ECONOMICS

3/26/20262 min read

Before the equation, it helps to think intuitively.

Imagine you find something valuable — a house, for instance — but you are not ready to commit. Instead, you pay for the right to buy it later at a fixed price. You are not obligated to follow through; you are simply preserving a possibility.

This is what an option does.

In financial terms, it is a contract that gives you the right — but not the obligation — to buy or sell an asset at a predetermined price within a given time frame.

It is, in a sense, a way of engaging with uncertainty without fully surrendering to it.

The question behind everything

For a long time, one question remained unresolved:

how do you assign a fair value to that right?

The instinctive answer was to rely on prediction — to estimate where the market would go and price accordingly.

But prediction is fragile. And building a system on fragile assumptions rarely leads to consistency.

The shift in thinking

What Fischer Black, Myron Scholes, and Robert Merton realized was deceptively simple, yet profound:

pricing does not require forecasting the future.

Instead, they showed that by combining an option with its underlying asset in carefully chosen proportions — a strategy known as delta hedging — one could construct a position that behaves as if it were risk-free.

And once something behaves like a risk-free asset, its return is no longer ambiguous — it must align with the risk-free rate.

From that point, the structure of the model follows with remarkable clarity.

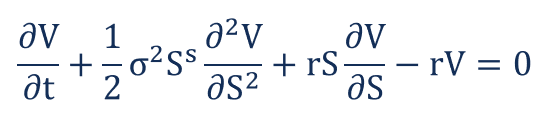

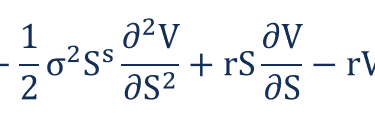

The formula

At first glance, it appears dense. In reality, it is simply a disciplined way of combining five elements:

the current price of the asset

the strike price

time

the risk-free rate

and volatility

Volatility is perhaps the most revealing component. It captures not direction, but dispersion — how much the future can deviate from the present. And in options, uncertainty itself carries value.

The terms N(d)N(d) translate this uncertainty into probability, grounding intuition in a statistical framework.

Why it changed everything

Before this model, options trading relied heavily on judgment and experience.

After its introduction in 1973, it became something far more systematic. The rise of the Chicago Board Options Exchangein the same year reflects this shift — theory and market evolving almost in parallel.

What is particularly interesting is that the model did not simply observe the market. It influenced it. As participants began to adopt its logic, prices themselves started to align with its structure.

It is a rare case where a theory does not just describe reality, but actively shapes it.

Where it falls short

And yet, like all models, it is built on assumptions.

It presumes constant volatility, continuous price movements, and frictionless markets — conditions that reality does not consistently provide.

Markets are discontinuous. They react, they overshoot, they destabilize.

The lesson here is subtle but important: mathematical elegance can guide decision-making, but it cannot replace judgment.

The deeper takeaway

What Black–Scholes ultimately offered was not certainty, but clarity.

It reframed uncertainty as something measurable, something that could be systematically incorporated into price.

And from that reframing, an entire financial architecture emerged — one that continues to shape how risk, time, and value are understood today.

Perhaps the most elegant aspect of all is this:

the breakthrough did not come from predicting the future more accurately,

but from realizing that, in this case, prediction was not necessary at all.

Some resources I recommend you to look:

Investopedia: https://www.investopedia.com/terms/b/blackscholes.asp

Veritasium:https://www.youtube.com/watch?v=A5w-dEgIU1M

and its counter Fractal Manhattan:https://www.youtube.com/watch?v=s3oOJezMqm0

MIT open courseware: https://www.youtube.com/watch?v=2UCHztlWuZg

Khan academy:https://www.youtube.com/watch?v=pr-u4LCFYEY

Columbia University:https://www.columbia.edu/~mh2078/FoundationsFE/BlackScholes.pdf

Contact

Feel free to reach out for collaborations or questions.

irem.kalender@ug.bilkent.edu.tr

© 2026. All rights reserved.

www.linkedin.com/in/iremkalender7