İrem Kalender

From Unicorns To Zombies: How Zombie Ventures Occured

What is zombie startups and how they come to life? What was the opponents that drived unicorns to be zombies?

ECONOMICSBUSINESS

İrem Kalender

7/7/20267 min read

Over the past few years, a shift has been taking place across the global Venture Capital and startup ecosystem.

Some startups that achieved billion-dollar valuations in 2020 and 2021 and were known as "Unicorns" are facing different reality. Today, many of them are trapped in a state of financial purgatory neither growing nor entirely dying. They have become what the financial world nowadays calls Zombie Startups.

How an era of limitless, cheap capital created an army of the walking dead, look at the radical psychological shift among investors, and explore the ecosystem's new economic reality?

Growth at All Costs strategy hasn’t bear its fruits

If we look at the past where everything started especially in times of low interest rates approaching zero, capital was cheap , public markets offered measly yields, forcing institutional investors to look elsewhere. Venture capital, with its promise of exponential tech growth, became the ultimate destination for cheap capital seeking outsized returns.(Mallaby, 2022) and many tech startup were alligiable to have this cheap capital investment. Driven by an intense Fear of Missing Out (FOMO), investors were aggressively deploying capital, desperate not to miss the next big thing.

Back then, many people measured a startup’s success by only Growth Rate. Since:

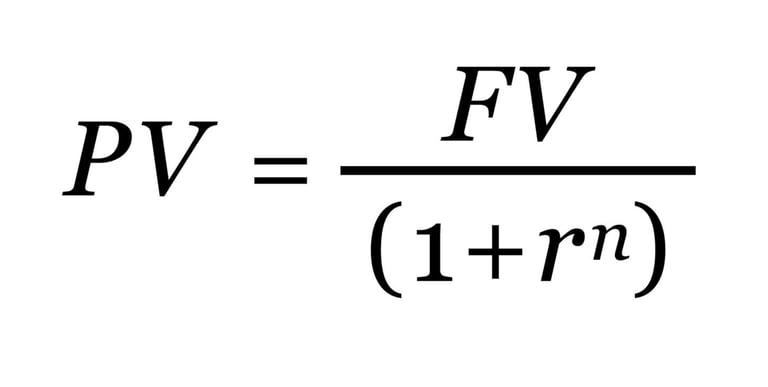

· The Mathematics of Low Discount Rates (r):

When the market interest rate approaches almost zero the Money you deposit today and after 15 years means almost the same thing

Hence investors wanted something can yield more even though if it is distant since impact of interest was almost zero it would be more profitable even taking considiration of the cost of time. Therefore it was appropiate for looking growth rate rather than other factors since the markets had a constant behaviour of low interests.

· Winner takes it all Dynamics and Network Effects

Most of the ventures back then (in zero interest rate period) fintech, software, or social platforms these platforms has a common feauture of network effects meaning they are getting more valuable as the users are increased.

In these type of market the late you are the more you miss. In network markets, consumers are willing to pay a premium for a larger network, so a platform that can establish an early lead can leverage a self-reinforcing cycle. As a result, network markets tend to be 'winner-take-all' arenas where a single platform dominates and runners-up are driven out or relegated to unsustainable niches. (Eisenmann et al., 2006) Since competition was wild when a company stoped growing the other company would take its place with anaother venture New entrants penetrate the market using disruptive innovations, establishing a strong position and eventually overtaking the incumbent before it can pivot its resources to a new venture (Christensen & Raynor, 2003)

· Not needing profits

Normally for a company to run, operate, and live they should make some profit. Other wise company would go bankrupt but many VC s back then didn’t need massive profits to run

Since back then investors willing to deposit their Money in VC than banks since it was more profitable VCs actually didnt need to make profit since their equity was always positive and the resource was almost never ending. Hence they had the Money to operate whether they are making profits or not.

Rather than mainly profits for investors how efficiently their Money is used was more credential value since as long as the company grows the investors gain was bigger than if that Money would stay with low interest rates.

Companies that were unable to raise additional funding or could only do so at significantly lower valuations were forced to change their strategy. Instead of prioritizing rapid expansion, many focused on cutting costs and preserving enough cash to remain operational.

What exactly is a Zombie Startup

Zombie Startup is a company which claims to have continuing operations but which demonstrates little or no growth in product adoption, traffic, or revenue over consecutive quarters. (National Academy of Agricultural Research Management, 2024)

Companies that entered this stage typically adopted more of a survival approach. Their priority was no longer expanding, growth or innovation but having financial resources just enough to continue operating or recovering their own expanses until market conditions improved on the behalf of them. Zombie Startups generally share several common characteristics.

· Differentiation in valuations

Since after increasing interest rates eventually everything was getting more expensive the Venture funds dedicateded their time to winners rather than others capital was concentrated in fewer and larger transactions exceptional companies were able to raise very sizeable rounds on attractive terms, while capital formation remained heavily concentrated in established category leaders. (Chambers and Partners, 2026) Hence other companies were in their shadow in some way.

Demanded valuations based on realistic multiples of profit, not raw user growth.

Because founders and early investors refuse to take a "down round" (aka: raising money at a lower valuation, which heavily dilutes their equity and signals failure), they choose not to raise capital at all. Hence old valuation remained

· Burn rates

Now since funding became harder and more valuable investors not only should think twice but the change in their priorities has occured. They wanted:

· 100/10/1 rule

Since Cash inflows of these companies weren’t as strong as before asd investors weren’t willingly as before they needed profits now or to minimize their burn rates.

Many companies changed their strategies according to minimize their burn rate (aka: the velocity of a company consumes Money) they aggresively cut expenses, laid off staff, some halted their own marketting campaines.

By minimizing expenses they had come to a point where they were able to run and cover their own expenses but not to grow.

Whether a company was actually profitable or even sustainable often seemed almost irrelevant. Instead of focusing on fundamentals like unit economics or cash flow, investors were drawn to rapid, hockey-stick growth. With large amounts of funding available, many startups spent aggressively to capture market share, supported by valuations that were often disconnected from the underlying business.

However, when capital is easy to access, it can hide flaws in a company's business model for much long. creating the illusion of success through top-line growth while completely obscuring the fact that the venture's core economic assumptions are entirely unviable. (Christensen, 1997)

The Liquidity Drought

When inflation increased and central banks responded by raising interest rates, access to capital became much more limited now capital had a significant effect of time. As funding became harder to obtain, many of the factors that had been overlooked during the years of low interest rates investment became impossible to ignore.

Investors also began to change their priorities. Rather than focusing primarily on user growth, they increasingly asked whether startups had a clear path to profitability and more importantly was this a sustainable business model until the exit.

This shift marked the beginning of what many refer to as the "zombie startup" era. Since:

Aggressive cost reductions (Decreasing burn rate): Companies significantly reduce operating expenses by cutting marketing budgets, scaling back operations, and implementing layoffs. The main objective was to extend the available cash runway for as long as possible.

Stagnant growth: As investment in customer acquisition and product development declined, growth slowed or stopped altogether. Expansion plans were postponed, and innovation became a secondary priority. These companies generated enough revenue from their existing customer base to cover essential operating costs, such as salaries and infrastructure. However, without additional funding or meaningful profits, they lacked the resources needed to invest in future growth.

Limited operational sustainability: Since these companies are able to cover only their own crucial expenses they have a limited sources that they can use on operational investments that leads them almost no movement in operations even sometimes disruptions.

"Overall, zombie startups remained operational, but their focus shifted from creating long-term value to maintaining short-term survival. While this strategy allowed them to avoid immediate failure, it also limited their ability to innovate, expand, and remain competitive over time."

One of the most significant consequences of this period was the shift in investors' priorities. During the previous investment cycle, funding decisions were often driven by growth indicators and the expectation of future market dominance. As a result, startups with compelling visions were frequently able to have great amounts of investments despite having limited evidence of long-term financial sustainability.

As market conditions changed, investors became considerably more focused on financial performance rather than emphasizing growth potential alone, they increasingly evaluated startups based on quantative tangiable metrics and overall unit economics. These indicators became essential in assessing whether a business had a realistic path to profitability.

This shift reflects a broader change in the venture capital ecosystem. Instead of prioritizing rapid expansion at any cost, investors increasingly favor companies that demonstrate sustainable growth, operational efficiency, and a clear ability to generate long-term value.

Although the rise of zombie startups may appear to be a negative, it can also be viewed as part of the market's natural process. Periods of reduced funding tend to expose business models that depended heavily on external capital rather than on sustainable financial performance. As a result, resources are gradually reallocated toward companies with stronger fundamentals and more resilient business models.

This shift is also influencing the type of startups that attract investment. Rather than prioritizing companies focused only on rapid expansion, investors are increasingly supporting businesses that emphasize capital efficiency, sustainable growth, and long-term resilience. These firms are often referred to as "camel startups" because they are designed to withstand challenging market conditions while maintaining financial stability.

Overall, the recent changes in the venture capital market reinforce a fundamental principle of long-term success depends not only on generating revenue but also on achieving profitability, maintaining cash flow, and building a business model that can remain sustainable under even unpredictable economic conditions.

Works cited

Mallaby, S. (2022). The power law: Venture capital and the making of the new future. Penguin Press.

Eisenmann, T., Parker, G., & Van Alstyne, M. W. (2006). Strategies for two-sided markets. Harvard Business Review, 84(10), 92–101.

Christensen, C. M., & Raynor, M. E. (2003). The Innovator's Solution: Creating and Sustaining Profitable Growth. Harvard Business School Press.

Christensen, C. M. (1997). The Innovator's Dilemma: When New Technologies Cause Great Firms to Fail. Harvard Business School Press.

Chambers and Partners. (2026). Venture Capital 2026 Global Practice Guide: Industry Trends & Capital Deployment. Chambers and Partners Research.

National Academy of Agricultural Research Management. (2024). Startup Shabdkosh: A Compilation of Venture Capital, Incubator, and Innovation Domain Terms. AIDEA Innovations.

Image

Contact

Feel free to reach out for collaborations or questions.

irem.kalender@ug.bilkent.edu.tr

© 2026. All rights reserved.

www.linkedin.com/in/iremkalender7